National Cottage Market Outlook

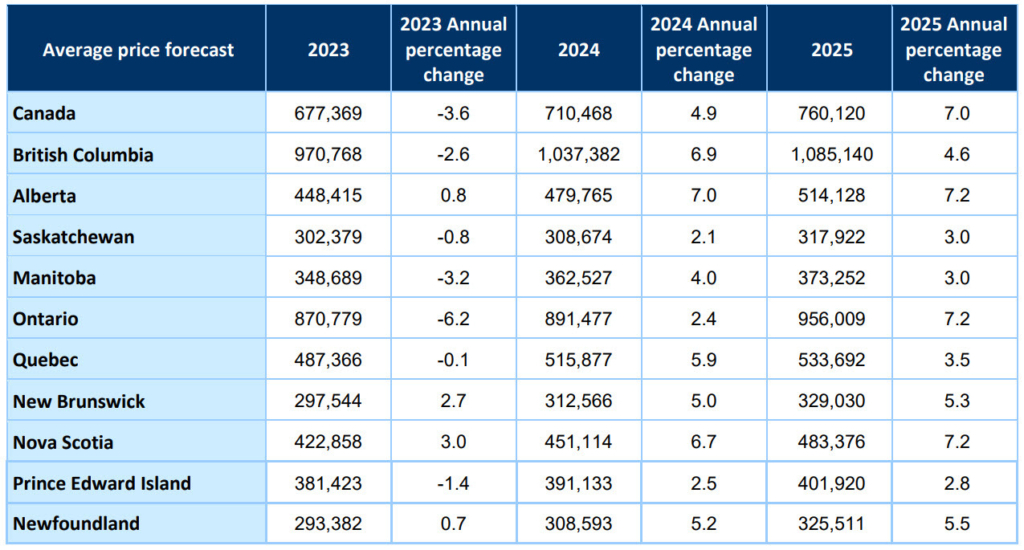

From a Canada-wide perspective, a flood of listings hasn’t hit the recreational property market this spring, and is unlikely to transpire this year. Despite the affordability challenges and higher interest rates that characterized the 2023 real estate market, Canada’s cottage owners are choosing to hold on to their properties in 2024 rather than selling off – a trend that’s likely influenced by the desirable quality of life alongside the prospect of future returns on recreational property ownership. Looking ahead, RE/MAX brokers and agents in Canada are anticipating the national average cottage price to increase 6.8 percent. Meanwhile, the number of sales is expected to rise in the majority of regions analyzed (61.9 percent), increasing between three percent upwards of 50 percent this year.

Cottage prices have increased in 83 percent of Western Canada’s recreational markets, according to RE/MAX Canada’s 2024 Cottage Trends Report. Year-over-year gains were noted in Whistler (+7.5 percent, from $1,633,855 in Q1 of 2023 to $1,756,473 in Q1 of 2024); Tofino (+100 percent from $0 in Q1 in 2023 due to no available inventory, to $1,001,116 in Q1 of 2024); Edmonton Lakes (+11.8 percent, from $639,750 in Q1 of 2023 to $715,300 in Q1 of 2024**); Canmore (+8.1 percent, from $962,619 in Q1 of 2023 to $1040,422 in Q1 of 2024); and Sylvan Lake and Central Alberta (+14.9 percent, from $580,357 in Q1 of 2023 to $666,949 in Q1 of 2024). Meanwhile, Ucluelet experienced a decrease in sales price (-11 percent, from $764,000 in Q1 of 2023, to $676,703 in Q1 of 2024). North Okanagan also saw a decline in price (-12 percent, from $835,193 in Q1 of 2023, down to $739,000 in Q1 of 2024).

According to RE/MAX brokers’ outlook for the remainder of the year, Western Canada’s cottage prices could see average prices rise between five and 10 percent, as demand continues to grow. Price is expected to increase by two percent in North Okanagan, five percent in Edmonton Lakes, Sylvan Lake and Central Alberta, 10 percent in Canmore and 10 percent in Ucluelet. On the flip side, Tofino is anticipating a 10-per-cent decrease in sales prices due to regional limitations on short-term rentals this year, which is prompting some recreational property owners to divest themselves of their properties or convert them into primary residences.

Compared to 2023 market conditions, Central Alberta, as well as Sylvan Lake and Canmore continue to favour sellers, while Edmonton Lakes is experiencing a more balanced market. Whistler, British Columbia is also gaining balance, with an eight-per-cent listings-to-sales ratio for single-family homes, compared to 30-per-cent listings-to-sales ratio for affordable condominiums. Tofino and Ucluelet on the other hand, have shifted from a balanced market to a buyer’s market.

Similar to 2023, retirees are driving recreational property sales (notably in Canmore, Edmonton Lakes and Central Alberta) followed by families (in Canmore, Central Alberta, Tofino and Ucluelet), couples (in Edmonton Lakes, Central Alberta, Tofino and Ucluelet) and investment buyers (in Canmore, Central Alberta, Tofino and Ucluelet). Favoured amenities among buyers in these regions include access to recreational activities (most notably in Canmore, Edmonton Lakes, Central Alberta, Whistler, Tofino and Ucluelet), followed by functional WiFi access (in Edmonton Lakes, Central Alberta, Whistler, Tofino and Ucluelet), proximity to water (in Edmonton Lakes and Central Alberta), close-knit communities (in Tofino and Ucluelet), and swimming pools (in Canmore and Whistler).

Four out of the 7 regions analyzed in Western Canada have recorded a sales increase in the first quarter of the year, including Whistler (+2.6 per cent, from 114 in Q1 of 2023 to 117 in Q1 of 2024); Tofino (+300 percent, from zero sales in Q1 of 2023 to three in Q1 of 2024); Edmonton Lakes (+27.8 percent, from 18 in Q1 of 2023 to 23 in Q1 of 2024**); and Canmore (+19.8 per cent, from 101 in Q1 of 2023 to 121 in Q1 of 2024). Meanwhile, sales in Ucluelet have held steady year-over-year (six in Q1 of 2023, and six in Q1 of 2024), while sales declined in North Okanagan (down seven percent, from 15 sales in Q1 2023 to 14 sales in Q1 2024), as well as in Sylvan Lake/Central Alberta as a direct result of inventory shortages (down eight percent, from 40 in Q1 of 2023 to 37 in Q1 of 2024).

Much in line with the Leger survey data, brokers in Western Canada, with the exception of Tofino, also reported that recreational property owners continue to hold onto their properties and aren’t offloading as a result of affordability. Sales decisions are more likely being driven by downsizing and aging out of the property.

**Edmonton Lakes sale price figures and number of sales figures are inclusive of data collected from residential and lakefront property transactions.

Market-By-Market Overview

WHISTLER, BC

Whistler’s residential property market is currently balanced across all property types, with activity being driven by a mix of families, couples (young, middle-aged), retirees, investment buyers, foreign buyers and out-of-province buyers.

The 2024 average residential sale price across all property types increased by 7.5 percent year-over-year (from $1,633,855 in Q1 2023 to $1,756,473 in Q1 2024). Average number of sales increased by 2.6 percent year-over-year (from 114 in 2023 Q1 to 117 in 2024 Q1).

For single-family homes (chalets), Whistler is currently deep in buyer’s market territory with an eight-per-cent listing-to-sales ratio, while in the lower price points (condominiums), Whistler is experiencing a seller’s market, with a 30-per-cent listings-to-sales ratio.

Buying & Selling in Whistler

Buyer demand is strong when it comes to residential properties. Pricing and number of sales have ticked up year-over-year; however, current interest rates are capping purchasing power, which is in turn causing different segments of the residential market to react differently.

Most buyers in Whistler are hailing from the Greater Vancouver Area and local to Whistler, with about six percent coming from elsewhere in Canada and eight percent coming from the US. The features and amenities most in demand among residential property buyers in Whistler are:

Regulations are having an impact in the region. For example, new mandates from the provincial and federal governments concerning the number of dwellings on properties zoned for single-family homes are expected to have an influence on the value of vacant lots and single-family home properties in certain price points. Exactly how this will play out with the municipality specifically, remains to be seen. Changes are anticipated to take effect starting after June 30.

Advice for Buyers

-

It’s advisable for buyers to determine with their real estate agent which features are the most important to them. This will help stay organized and ready to go when their desired property hits the market.

-

For sellers, pricing their property correctly is paramount to achieving a sale in the Whistler market. A professional broker can walk them through the proper pricing methodology and a strategy which best suits their needs.

-

One persisting trend from the pandemic seems to be the relatively low number of properties on the market at any given time. A strong desire to live, work and play in the beautiful area of Whistler, combined with a shortage of properties on the market, has kept the number of listings low.

TOFINO & UCLUELET, BC

Tofino & Ucluelet are experiencing a buyer’s market, due to new capital gains increases from the federal government and the short-term rental rules imposed by the BC Government. Tofino, although exempt as a resort municipality, has chosen to opt into the provincial legislation. Ucluelet, on the other hand, has continued to opt out.

Families, couples (including young and middle-aged) and investment buyers are driving the residential and recreational property sales. This trend is expected to continue.

In Tofino, there were no sales or listings inventory recorded in Q1 2023. But, in Q1 2024, the average recreational sale price was $1,001,116. The number of sales across all recreational properties in the region increased by 300 percent year-over-year (from 0 in Q1 2023 to 3 in Q1 2024).

In Ucluelet, the average cottage prices across all recreational properties decreased by eight percent year-over-year (from $764,000 in Q1 2023 to $676,703 in Q1 2024). The number of sales held steady year-over-year (6 in Q1 2023 and 6 in Q1 2024).

Average sale prices and transactions are expected to decline 10 percent in Tofino through the remainder in 2024. Meanwhile, Ucluelet will likely see both sales and prices rise by 10 percent.

Buying & Selling in Tofino & Ucluelet

Despite inventory increasing in the region, short-term rental rules are creating challenging conditions for investors and buyers seeking additional income through short-term stay rentals. This is expected to be further pressured by the federal’s government’s capital gain tax increase which will go into effect on June 25, with many owners looking to sell and close before that date. Some property owners have chosen to list their property, prompted by the federal government’s announcement of a capital gains tax increase.

Buyers are coming from the lower mainland and Vancouver Island. This has not changed since last year. The features and amenities most in demand among residential property buyers in 2024 are:

Regulations such as short-term rentals are impacting the local residential markets. Tofino has opted into the new provincial legislation restricting short-term rentals. Tofino property owners with affected properties are likely to see a significant drop in value as income will be about 1/3 or less of what they were earning as short-term rentals. Ucluelet has managed to deal with short-term rentals issues by zoning and has chosen to opt out of the provinces short-term rental rules. Ucluelet is likely to see more buyers who would have otherwise considered Tofino.

Advice for Buyers

-

Sellers need to keep in mind that with higher interest rates, the market is not what it was in 2020 and 2021. There are fewer sales and less competition.

-

Buyers need to be mindful of the shifting landscape and to ensure they do a thorough job understanding what short-term rental restrictions apply.

EDMONTON LAKES, AB

Edmonton Lakes’ property market is currently balanced, with the spring season generally affording enough inventory for six months of sales. Couples, including young and middle-aged couples, and retirees, are driving property sales.

The 2024 average residential sale price across all residential property types, not including lakefronts (Zones 75,71 & 93) increased by 22.7 percent year-over-year, from $388,772 in Q1 2023 to $477,104 in Q1 2024. Meanwhile, the average price of lakefront properties (Zones 75,71 & 93) increased by 10.5 percent, from $639,750 in Q1 2023 to $715,300 in Q1 2024.

The number of sales increased by 27.8 percent year-over-year (from 18 in 2023 Q1 – of which 4 were lakefronts, to 23 in 2024 Q1 – of which 10 were lakefronts).

Prices are anticipated to increase by five percent by the end of the year – depending on the inventory on the market. Sales will likely remain balanced year-over-year, with a possible slight increase of up to three percent by end of 2024.

Buying & Selling in Edmonton Lakes

Edmonton Lakes is starting to see newer homes coming on the market that generate a higher value, which is contributing to the increase of the sales price values. Inventory is generally fairly stable with the major market season beginning in April of every year until around the end of October.

Most buyers are coming from both out-of-province (BC and Ontario), and locally, from Edmonton and Edmonton’s surrounding area, and Northern Alberta. This has not changed since last year.

The features and amenities most in demand among buyers in 2024 include:

Since the onset of COVID-19, buyers continue to want out of city centres while taking advantage of lower interest rates. They can enjoy the quality of life that the ‘lake life’ offers. It also helps that the Edmonton Lakes region is only an hour out of the city of Edmonton, making it easy to commute.

Advice for Buyers

Hire a local expert in the desired local target area. Local expertise helps ensure buyers get what they are looking for.

CANMORE & BANFF, AB

Canmore/Banff is experiencing a seller’s market, as it continues to struggle with lack of inventory and low buyer demand. Families, couples (including young and middle-aged couples), retirees and investment buyers are all driving residential property sales in the region. Albertans are also driving property sales in the region. This trend is expected to continue.

The 2024 average residential sale price across all residential property types increased by 8.1 per cent year-over-year, from $962,619 in Q1 2023 to $1,040,422 in Q1 2024. Sales across all residential property types increased by eight per cent year-over-year, from 101 in 2023 Q1 to 121 in 2024 Q1.

Average cottage prices in the region are likely to increase by 10 percent by the end of 2024, while sales is likely to increase by five percent.

Buying & Selling in Canmore & Banff

There continues to be strong buyer demand, mainly from Alberta and Ontario. In addition, there is international demand, though they can’t currently purchase. Lack of supply is putting upward pressure on pricing. Much like 2023, strong demand for properties which are eligible for nightly and weekly rental is also trending in the region.

Out-of-province buyers are coming from Ontario, and more-locally from Calgary and Edmonton. This has not changed since last year. The features and amenities most in demand among residential property buyers in 2024 are:

Advice for Buyers

-

Be prepared to act quickly.

-

Be prepared to compete for properties.

-

Although this is a seller’s market, there is still a need to price correctly to successfully sell.

SYLVAN LAKE, AB

Central Alberta Lakes’ residential property market is currently a seller’s market, driven by strong demand and short supply. The Alberta economy is very strong, with population increases due to inter-provincial migration from Ontario and B.C. New construction isn’t keeping up with demand driving prices higher. Families, retirees and investment buyers (for Airbnb) are driving property sales. This trend is expected to continue, so long as Central Alberta’s economy stays strong.

The 2024 average recreational sale price across all recreational properties increased by 14.9 percent year-over-year, from $580,357 in Q1 2023 to $666,949 in Q1 2024. Sales decreased by 7.5 percent year-over-year, from 40 in Q1 2023 to 37 in Q1 2024.

Looking ahead, average prices are anticipated to increase by five percent by the end of 2024, while total sales will likely decline by by three percent.

Buying & Selling in Sylvan Lake

There are fewer recreational properties on the market with continued strong demand, although high interest rates are probably slowing sales somewhat. Average 91 days on market in the first quarter of 2024, compared to 78 days in the first quarter of 2023.

Most buyers are coming from both out-of-province (Ontario and B.C.), and locally, from Calgary and Edmonton. This has not changed since last year. The features and amenities most in demand among buyers in 2024 include:

-

Large properties with more outdoor/green space

-

Waterfront properties

-

Access to recreational activities (i.e. skiing, water sports)

-

Good Wi-Fi access

Since COVID-19, there is a strong Central Albertan economy with lots of money around which allows families to make discretionary spending decisions. Supply of lake property in Alberta is limited, driving prices higher when the economy is strong.

Advice for Buyers

There are still properties available at relatively affordable prices at the less popular lakes, including: Pine Lake, Buffalo Lake and Gull Lake. Although, they are all suffering from lower water levels due to the drought in Alberta.

Courtesy RE/MAX LLC